The last few years have seen a massive drop off in the importance of traditional storage systems, culminating in the market leader (EMC) being acquired by Dell in 2015. Spending on hardware has dropped from $45b in 2011 to $33b in 2018 (see my Figure above). Shipments on the other hand have increased to reach their highest ever volume (907k) due to the introduction of cheaper arrays such as Dell EMC’s vxrack and vxrail and the growing use of storage software to improve the usability of installed arrays. Read more »

The last few years have seen a massive drop off in the importance of traditional storage systems, culminating in the market leader (EMC) being acquired by Dell in 2015. Spending on hardware has dropped from $45b in 2011 to $33b in 2018 (see my Figure above). Shipments on the other hand have increased to reach their highest ever volume (907k) due to the introduction of cheaper arrays such as Dell EMC’s vxrack and vxrail and the growing use of storage software to improve the usability of installed arrays. Read more »

Huawei v Cisco vie for control of the $181b network market

The network market is one of the most vital of all ITC areas, as it enables the connection between devices in a world in which it seems everything is being computerised. Partially due to this important role as well as its beginnings in the telecoms world, it is one in which national suppliers are still battling for dominance. It is hardly surprising therefore that this market is being deeply affected by the growth of new nationalism and trade wars between the USA and China. My Figure above shows the 2018 market shares of the leading suppliers split between enterprise and (the much larger) service provider network markets. Read more »

ITCandor celebrates 10 years – Thank You All!

Dear Reader

Today ITCandor is celebrating its first 10 years of operations. During that time I have:

- Published 850 research papers, which have been read by half a million;

- Analysed and forecasted the world IT and communications markets each quarter;

- Partnered with many other research agencies, both large and small;

- Attended hundreds of industry events in person and

- Helped many vendors and users with their business planning.

I’ve spoken at many industry events and enjoyed debating the latest and most important issues with hundreds of executives, users and analysts.

Looking forward I see a growing role for the company as ‘new nationalism’ starts to affect go-to-market strategies in what otherwise is the most global of all… and we come to terms with the computerisation of everything and the ethics of the algorithms and AI that control them.

I want to thank everyone who has helped along the way and look forward to many more years of working in this fabulous industry.

Martin

IBM Q1 2019 storage announcements – security and AI for hybrid multi-cloud customers

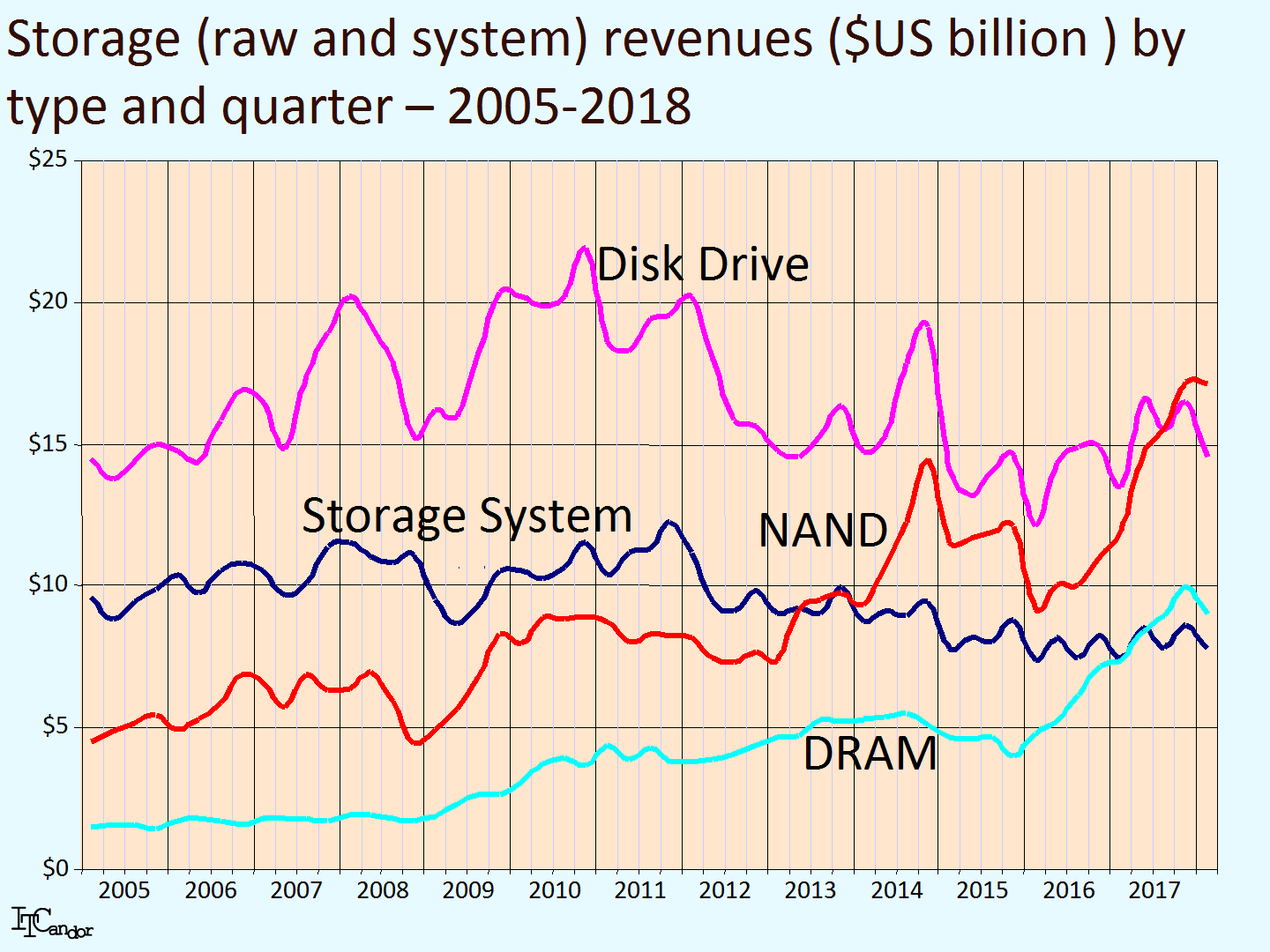

Computer data is becoming increasingly important (see my Figure for the capacity growth of disk, NAND and DRAM devices) and difficult for users’ organisations to plan, manage and defend.

IBM, like other storage systems suppliers, has recognised this growing importance through embracing Software Defined Storage (SDS), while constantly adding new technology (such as NVME drives and non-IBM storage protocol connectors) and features to give its users the maximum amount of control over what might otherwise be an insurmountable problem. In this post I describe IBM’s latest additions and enhancements and how they help its customers. Read more »

{kind=link}

HPE’s Composable Cloud – software-defined-everything future systems

Antonio Neri took over as HPE’s CEO in February last year. Since then we’ve seen some senior management changes and a refocusing of the company’s messaging. HPE is one of the most important suppliers of enterprise IT equipment – second to Dell EMC in servers, third in storage systems behind Dell EMC and NetApp and third behind Cisco and Huawei in enterprise networks (see my Figure). It is also one of the largest suppliers of enterprise systems management software. Its OneView offering – retained when most of its software was offloaded to Micro Focus in 2017 – is widely used by large organisations, especially in government, manufacturing and telco sectors. Read more »

Antonio Neri took over as HPE’s CEO in February last year. Since then we’ve seen some senior management changes and a refocusing of the company’s messaging. HPE is one of the most important suppliers of enterprise IT equipment – second to Dell EMC in servers, third in storage systems behind Dell EMC and NetApp and third behind Cisco and Huawei in enterprise networks (see my Figure). It is also one of the largest suppliers of enterprise systems management software. Its OneView offering – retained when most of its software was offloaded to Micro Focus in 2017 – is widely used by large organisations, especially in government, manufacturing and telco sectors. Read more »

DevOps – trends and choices

Every computer systems in use has operational and development functions associated with it. In enterprises with their own data centres, these are often separated between those that keep the systems running (operators) and those that write applications (developers). DevOps is a term used to describe a software development methodology which combines software development with IT operations. It is different from, but associated with, other terms such as Agile project management, ArchOps, continuous delivery, DataOps, DevSecOps, site reliability engineering, systems administration and WinOps. The challenge for modern IT organisational structures is how to get these two teams to work on the same side rather than in conflict with each other. Read more »

Every computer systems in use has operational and development functions associated with it. In enterprises with their own data centres, these are often separated between those that keep the systems running (operators) and those that write applications (developers). DevOps is a term used to describe a software development methodology which combines software development with IT operations. It is different from, but associated with, other terms such as Agile project management, ArchOps, continuous delivery, DataOps, DevSecOps, site reliability engineering, systems administration and WinOps. The challenge for modern IT organisational structures is how to get these two teams to work on the same side rather than in conflict with each other. Read more »

Your copy of ITCandor 2019 predictions pdf

Please send an email with your name and company to info@itcandor.com and I’ll send you a pdf of this year’s predictions.

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

Is Apple over-dependent on China and iPhone?

Apple’s CEO Tim Cook issued a revenue warning at the beginning of January, indicating that revenues in Q4 had declined 5% to $84 billion. He added more information on positive growth items such as services, iWatch and the Americas. At almost any other time in our industry his announcement would have been unusual, but we live in volatile days. Apple is the largest supplier in the world, dwarfs every other ITC vendor in both revenues and net profit (see my Figure for its annual progress in both since 2003) and has been buffeted by its stock market valuation since just before Xmas along with others such as Facebook, Google and eBay. The early analysis reported on the TV and radio suggested that its business may be over-dependent on China as a region and its iPhone as a product. I want to add a bit more detail from my on-going research. Read more »

ITCandor celebrates 10 years of ITC industry predictions

PRESS RELEASE – Didcot, January 3rd, 2019

ITCandor’s predictions ’10 by 10′ landmark

ITCandor has published its 10th set of annual predictions

ITCandor has reached the landmark total of 100 predictions covering each year from 2009 to 2019. That’s 10 consecutive sets.

For budding historians, here’s a list of them all.

I’ve assessed the accuracy of each set as well of course and presented them many times across the globe. I’d like to thank all of those customers, friends, colleagues and contacts who’ve helped, criticised and encouraged me throughout.

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

ITCandor publishes its 2019 predictions

PRESS RELEASE – Didcot, December 31st, 2018

ITC in 2019 – culture clashes and trade wars

ITCandor has published its 10th set of annual predictions. These are the 10 ideas for the ITC industry in 2019: Read more »

ITCandor’s 2019 ITC predictions – culture clashes and trade wars

Welcome to my 10th set of annual predictions for the IT and Communications (ITC) industry. As always I began with a self-assessment of last year’s efforts. Read more »

Welcome to my 10th set of annual predictions for the IT and Communications (ITC) industry. As always I began with a self-assessment of last year’s efforts. Read more »

The market grows by just 0.8% worldwide – EMEA continues to fall behind

2018 was a good year for the IT and communications industry. My forecast (based on actual results up to September) suggests that spending grew by 4% to $6.5 trillion. Net profit for the industry’s suppliers will also have flourished, growing 13% to $785 billion, an abnormal extension of the 23% growth in 2017. Total industry headcount grew by 3% to 19.7 million – an all-time high despite the increasing use of AI and ML by suppliers.

2018 was a good year for the IT and communications industry. My forecast (based on actual results up to September) suggests that spending grew by 4% to $6.5 trillion. Net profit for the industry’s suppliers will also have flourished, growing 13% to $785 billion, an abnormal extension of the 23% growth in 2017. Total industry headcount grew by 3% to 19.7 million – an all-time high despite the increasing use of AI and ML by suppliers.

In 2019 I expect less growth all round; spending growth will be just 0.8% to $6.7 billion, net profits will decline by 0.3% and industry employment will grow by 1.0%. My rationale is that increasing nationalism (Trump, Brexit, Catalonia, etc.) will limit trade. It is highly unlikely that significant manufacturing operations will move away from the Far East (and particularly China, Taiwan and South Korea) to the US or Europe – we’re just too globalised and labour costs remain too advantageous.

Spending growth at a regional level in the Americas (+1.4%) and Asia Pacific (+1.2%) will both be better than EMEA, where it will decline by 0.3% (see my Figure).

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

ITC manufacturing stays in the Far East despite new nationalism

Trump, Brexit, Catalonia,… I’ve been reporting for a few years now on the rise of new nationalism and extreme politics and how it affects the ITC industry. Politicians use phrases such as ‘fake news’ and ‘project fear’ to silence debate, often ignoring the realities of the workings of the global economy. One important issue for the nationalists is the source of the products we buy. Our industry is arguably the most global of all and we’ve seen a constant move of manufacturing to the Far East.

Trump, Brexit, Catalonia,… I’ve been reporting for a few years now on the rise of new nationalism and extreme politics and how it affects the ITC industry. Politicians use phrases such as ‘fake news’ and ‘project fear’ to silence debate, often ignoring the realities of the workings of the global economy. One important issue for the nationalists is the source of the products we buy. Our industry is arguably the most global of all and we’ve seen a constant move of manufacturing to the Far East.

My Figure shows the consumption (top) of all ITC hardware by region, the nationality of the supplier (middle) and the manufacturing location (bottom), combining component and finished goods suppliers together and using the total amounts paid by the customer. It demonstrates a considerable disparity between the 3 dimensions. EMEA in particular has virtually given up on making computers and computer equipment, the Americas still dominate in terms of the the suppliers’ nationality; however they too have been exploiting lower wages and growing technical specialisation to use Far Eastern sub-contractors, or their own divisions to make the products they sell abroad.

Nationalists need to decide where their products should be made (at home or abroad) and by whom (by a national supplier or not). In the US almost all ITC suppliers are making their equipment abroad, so Trump is trying to provide incentives for indigenous manufacturing. In the UK, although it is already too late for the ITC industry, politicians ought to encourage the creation of major UK manufacturers, especially in the car market where there are none.

The growth of our market will be curtailed significantly if the trade wars and new tariffs are expanded to cover services as well as manufactured goods.

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

Cyber security goes multi-tenant and cross-border

Cyber security is an increasing challenge for all individuals and organisations; the threat landscape is expanding as national governments join the long list of antagonists aiming to create breaches and chaos and we’ve got beyond the point at which ITC networks can be protected by applying just signature-based software and processes. Larger organisations have deployed Security Operations Centers (SOCs) to manage the issues, but skilled security specialists are expensive and increasingly difficult to find. The solution has been to employ Managed Security Service Suppliers (MSSPs) to provide tools and help with identifying vulnerabilities and remediation of successful attacks. However these services are also expensive as their suppliers apply significant people resources to be successful.

Cyber security is an increasing challenge for all individuals and organisations; the threat landscape is expanding as national governments join the long list of antagonists aiming to create breaches and chaos and we’ve got beyond the point at which ITC networks can be protected by applying just signature-based software and processes. Larger organisations have deployed Security Operations Centers (SOCs) to manage the issues, but skilled security specialists are expensive and increasingly difficult to find. The solution has been to employ Managed Security Service Suppliers (MSSPs) to provide tools and help with identifying vulnerabilities and remediation of successful attacks. However these services are also expensive as their suppliers apply significant people resources to be successful.

In 2019 I expect to see a significant growth in the use of Managed Detection and Response (MDR) services as a cheaper – and sometimes more efficient – solution for the growing problems. MDR suppliers all use AI and ML (albeit in different ways) to monitor and sometimes remediate attacks. Their services are based on sharing threat intelligence across multiple countries and SOCs to widen the ability of organisations to protect themselves.

In the Figure I compare the relative values of MSSP and MDR services across a number of criteria. MDR will grow in medium-sized countries that allow their log data to be exporter across country borders and share in an anonymous way for protecting others. These include the UK (paradoxically given its decision to leave the EU), Nordic countries, the Netherlands and Australia amongst others. The US market itself is so large that almost all cyber security services can be based in-country. The inhibitor of MDR growth is the cultural reticence of organisations in certain countries such as Germany, France and Italy to allow the cross-country movement of log data.

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

The EU suffers post-Brexit blues

I expect ITC spending to decline by 0.3% in EMEA in 2019, but EMEA itself is divided into a number of sub-regions (see my Figure). I expect both Western (-0.5%) and Eastern (-0.2%) Europe to fare worse than Africa (+0.9%) and the Middle East (+1.0%) in the year.

I expect ITC spending to decline by 0.3% in EMEA in 2019, but EMEA itself is divided into a number of sub-regions (see my Figure). I expect both Western (-0.5%) and Eastern (-0.2%) Europe to fare worse than Africa (+0.9%) and the Middle East (+1.0%) in the year.

The major issue affecting ITC spending in the whole region will be how the EU manages to resolve growing trade challenges. It has failed to create regional champions in our industry, so almost all hardware and software used by its citizens and companies are now sourced from suppliers based in the Americas or Asia Pacific. ITC products are likely to become more expensive in the EU as the result of trade wars between the US and China; in the absence of its own regional suppliers it makes no sense to engage in its own trade wars.

The UK has been a strong asset to the EU as it has been the traditional first staging post for ITC suppliers seeking to expand across the region. As the UK leaves the EU is left with only one country (Ireland) that speaks English as its national language. While the UK market will decline most of all countries in EMEA in 2019, the ITC market in remaining EU states also face a less certain future as a result.

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

Cloud wash 2019 – investment costs spiral; the bubble bursts for some

Infrastructure and Platform as a Service (IaaS and PaaS) will continue to be the strongest growing IT services offerings in 2019, growing 20% and 22% respectively (see my Figure). However I expect to see increasing challenges for their suppliers in the year. In particular:

- Investment costs will increase as suppliers build more data centers in their expansion into new countries and regions and as new processor chips from Intel, AMD and others reduce the cost advantages of their older ones.

- New nationalism and cultural reticence to use foreign data resources will increase.

- Business plans for new suppliers will be restricted by national and region uncertainties and legislation.

- The fall in stock market valuations of leading hyperscalers at the end of 2019 demonstrates investor nervousness in a market that has given them strong returns since its inception.

Cloud computing in 2019 will no longer be so special and I expect to see an increase in ‘cloud washing’ – criticism by users and analysts that it has failed to live up to its (previously unlimited) potential. A few suppliers may even become ‘over-hyperscalers’!

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

Large organisations adopt multi-cloud management for better data governance

My long-term forecast is for infrastructure software and cloud services to replace more traditional outsourcing and managed services in the ITC market over time. However in 2019 most large organisations have already experimented with cloud computing as a replacement for running their own systems and are looking to do more. As the initial hype of cloud computing recedes I expect a number of changes. In particular:

My long-term forecast is for infrastructure software and cloud services to replace more traditional outsourcing and managed services in the ITC market over time. However in 2019 most large organisations have already experimented with cloud computing as a replacement for running their own systems and are looking to do more. As the initial hype of cloud computing recedes I expect a number of changes. In particular:

- The introduction of the EU’s GDPR legislation has made a major change and makes having a ‘single version of the truth’ for all databases and necessity as opposed to a ‘nice to have’… and even if you’re not based in the EU you’ll need to become compliant in order to continue to do business with EU customers.

- Each cloud supplier’s offerings are different from each other, so you’ll need to manage your resources separately for AWS, Azure, Google Cloud, IBM Cloud and each of the others.

- Ideally you’ll be able to monitor the usage of your resources, making (sometimes ‘on the fly’) decisions to utilise external services to expand at peak usage times, and/or save money by moving processing to cheaper systems, whether you own them or not.

Each cloud service comes with a completely different set of protocols and tools from the ones you’ve been using in-house for your physical and virtualised infrastructure. Using APIs companies such as

- IBM, Dell EMC and NetApp are already providing data storage management for a widening spread of heterogeneous systems,

- Vmware has announced a number of partnerships with the leading cloud suppliers to help hypervisor-based virtual applications to bridge the gap between on-premise and cloud platforms, while

- Docker and others help with the integration of container-based applications.

Whether or not the management software for each environment is good or bad, you’re workload will be more if you have to run each of them separately. In consequence I believe that 2019 will see significant success for suppliers who address and allow multiple environments to be managed in a converged way.

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

IT and OT convergence will be limited by differences in expectations and market views

For as long as I’ve been an analyst the markets for general purpose and industrial computing have been separated; back in the early 1980s IBM used to call the latter Non-Commercial Area Systems. The 2 areas require different technical expertise, as was demonstrated when HP even split out Agilent (its process-control arm) in 1999. Today perhaps the best way of looking at them is to think of Information and Operational Technology (IT and OT).

For as long as I’ve been an analyst the markets for general purpose and industrial computing have been separated; back in the early 1980s IBM used to call the latter Non-Commercial Area Systems. The 2 areas require different technical expertise, as was demonstrated when HP even split out Agilent (its process-control arm) in 1999. Today perhaps the best way of looking at them is to think of Information and Operational Technology (IT and OT).

In recent years the ever-increasing power of microprocessors, improvements in wireless and other networking protocols and massive advances in memory and solid state disk capacities have inspired an number of innovators to create new products, loosely coupled together under the banner of Internet of Things (IoT). My Figure is a photograph of Google’s experimental self-driven car, but there are a huge number of other types of device being created mainly by manufacturing companies for deployment in Smart Cities, for health monitoring and other applications.

While I have many personal reservations about my own use of many of these new devices – I like driving and would prefer to keep my activities private – we appear to be running headlong into a world full of them.

My prediction however is that 2019 will be a time when the reality of the differences between IT and OT will slow their integration. In particular:

- Purchasing life cycles are very different, with IT components and systems being replaced far more rapidly than OT ones.

- The reliability of some OT equipment has to be much greater than for general purpose IT; transportation, medical and industrial equipment can kill people if they go wrong.

- There is a need to classify and filter monitored data from OT before it can be successfully included into IT management systems.

I’m not sticking my head in the sand here – just pointing out that the excitement many feel when new devices and process are first described will be limited by the years of hard work technologists will need to do to get them to work… and that we may be bored of some of them by the time they eventually arrive.

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

European and Japanese suppliers fall behind US and Chinese ones

I’ve already talked about the shift in the manufacturing of ITC equipment to the Far East in my second prediction. When it comes to the whole ITC market (including hardware, software, IT and telecoms services) there has been an ongoing shift towards Japanese and US-based suppliers as well as those from other – mostly Far Eastern – countries (see my Figure).

I’ve already talked about the shift in the manufacturing of ITC equipment to the Far East in my second prediction. When it comes to the whole ITC market (including hardware, software, IT and telecoms services) there has been an ongoing shift towards Japanese and US-based suppliers as well as those from other – mostly Far Eastern – countries (see my Figure).

In 2019 I see no reason why this trend won’t continue. It has significant implications for both Europe and Japan. The former has already run out of enough global suppliers to be able to influence the movement of the world market, while the latter is rapidly falling to the same position.

The biggest challenge for the suppliers (as well as almost all governments) is the relatively slow decision-making processes they employ and/or lack of appropriate investments. It seems no matter how hard Japanese and European suppliers speed up their decision making processes they continue to fall behind those from more advanced countries and they lack the support of relevant investors and government intervention to allow innovative new companies to take strong positions in new sub-markets. In Europe it is possible the EU could do something to combine the strengths of the telecoms suppliers (who remain principally national suppliers), otherwise it is too late. In Japan there is still considerable strength in robotics and gaming, but the larger full-range suppliers (Fujitsu, Hitachi, NEC, Sony, Olympus and others) look unlikely to continue to challenge at a global level.

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action

5G, SD WAN, NVMe over Fabric will drive ITC hardware growth

Most hardware sub-markets will decline in 2019 (see my Figure). Only processors and solid state disk (NAND and DRAM) will see significant growth, while the mobile device market will also grow (just). We have to turn to smaller sub-segments of these classes to pick out the real winners in the year. In particular:

Most hardware sub-markets will decline in 2019 (see my Figure). Only processors and solid state disk (NAND and DRAM) will see significant growth, while the mobile device market will also grow (just). We have to turn to smaller sub-segments of these classes to pick out the real winners in the year. In particular:

- 5G wireless networking will begin to be rolled out after a number of important trials run mainly in conjunction with Huawei. Sales of associated wireless cards (for computing and IoT devices) and base stations will help make up for the decline in other networking equipment to create a relatively level market in comparison with 2018.

- SD WAN implementations will continue to grow, which will also contribute to the network equipment market.

- NVMe over Fabric is an important new direction for the storage market, based on NVMe solid state drives which are built to communicate with processors at a much higher rate than older protocols such as SAS and SATA. In 2019 we will see a growth in SAN storage as a result of NVMe being applied to Fibre Channel and Ethernet. In turn this will bolster the overall storage systems, server and infrastructure software markets in the year.

Beyond hardware I expect IaaS and PaaS cloud services, security software and services (especially MDR) and systems management software to help drive their respective categories – see my Figure for a comparison of each of these below.

Navigate our predictions – intro 1 2 3 4 5 6 7 8 9 10

©ITCandor Limited – unauthorised copying of this content is illegal and will be rigorously defended by us through court action