You’re going to have to get your best reading glasses for this… I wanted to share the discrepancies in each country’s market growth for the year to the end of September 2014 and 2015. The Figure shows the differences ranked by growth in constant dollars. The data is for IT and Communications n total as discussed in my last paper.

It’s evidence of the continued dramatic fall of local currencies and the difficulty of trying to judge how the market is doing. In almost all cases local growth was significantly higher than $US dollar growth due to the constant devaluation of currencies. The prize for the most extreme difference goes to Russia where a 45.3% growth in Roubles was a 10.5% decline in dollars. As always please contact me if you want to learn more.

The ITC market falls 3.2% to $1.6T in Q3 2015

It’s not a great year for the IT and Communications market. Yet again we saw a fall in revenues – by 3.2% in the quarter to $1.6 trillion and in the year to the end of September of 4.4% to $6.0 trillion. Net profits also fell – by 4.3% to $173 billion and 28.3% to $630 trillion respectively. At the end of the quarter vendors employed a total of 17.8 million employees. As in previous years I’m working to publish my predictions for the coming year: for the moment it looks as if the market will fall by just 0.5%, which is much better than the likely all of 4.6% for 2015.

The figure shows the growth of the market by category. IT service – driven on by a significant growth in Cloud offerings – has been doing best followed by hardware: both software and telecom service have been performing badly. You’ll want to learn more about what happened in the last quarter. Read more »

Dell set to buy EMC – Wow!

For Sally….

Today Dell announced that it has made a $67B bid to buy EMC. In the last year this would have given the new company a market share of 2.0% of the total $3.8T IT market – jumping over Microsoft into fifth place.

You’ll want to learn more about the implications. In the Figure we combine the revenues of Dell, EMC and VMware to produce the shares for the proposed new company – named ‘Dell*’ here. See our earlier analysis of Dell’s strategy. Read more »

Business sector and consumer IT spending trends

I think it’s a good time to look at the development of the IT market by customer size and type, which is an essential feature of ITCandor’s market model. It’s especially important to look at the potential to grow market share by cut across from consumer to business markets. In fact, over the last 8 quarters consumer spending has been remarkably constant at around 34% in quarters 1-3, rising to 35% of total IT spending in the fourth quarter (see Figure). Small businesses (those with 100 or fewer employees) accounted for 33.6% of total spending in the year, followed by large companies (>1k employees) at 21.8%; leaving medium sized companies (those with 100 to 1k employees) with 10.2% of the spending. You’ll want to think more about market shares and industry sector spending we discuss below. Read more »

Currency consequences – the dollar keeps rising

Taking care of currency conversions is an essential job for an international market researcher and I’ve written about the process before. The US dollar keeps rising, making the value of spending in local measurements far in excess of current dollar value growth. As I begin to tackle the Q3 market I note that the changes have been even deeper than before. The Figure shows the growth of the $US against the deepest fallers for Q3 2015 v Q3 2014. China decided to lower its exchange rates recently, but remained one of the most stable. It’s interesting that some of the steepest falls have been in oil-rich countries, which are struggling to meet GDP targets due to sustained low prices.

Cloud services suffer massive regional currency discrepancies

Following my sizing and forecast for cloud services published yesterday, I wanted to expand on the regional growth stats. The rapidly falling value of almost all local currencies against the $US is making market planning very difficult at the moment, as many of you know only too well.

In the Figure I show the quarterly growth of revenues from cloud services (IaaS, PaaS and SaaS combined) in the Americas, Asia Pacific and EMEA. For the latter 2 regions I’ve shown growth in current $US (as per my previous sizing) and in local currency (¥ and €). Read more »

Cloud services – SaaS, IaaS and PaaS forecast

We sized the enterprise IT hardware market at $143b in a recent research paper. Now it’s time to look at cloud services – Infrastructure and Platform ‘as a Services’ are alternatives to building and maintaining your own data centre, while Software as a Service is an alternative to running application software within them. The Figure shows the quarterly development of the three cloud service types with a forecast to 2020. The total was worth $94b in the year to the end of June and will grow to be $206b by 2020 and – while the majority of this will be SaaS, there are clearly a shift going on in data centre ownership away from enterprise customers and towards service providers and software companies.

You’ll be interested to learn more about the market leaders and revenue trends and the consequences for your IT usage going forward. Read more »

PC market by product type – desktops aren’t dead!

A couple of weeks ago we looked at the world market for all client devices. I’ve been doing some work to split out various extra form factors in the mean time and am pleased to be able to publish some stats here on PCs. You’ll want to know more about how laptop, desktop, workstations and thin clients contribute to this vital part of the IT market. Read more »

IBM LinuxONE – new brand and aspirations in open source computing

Back in January we took a deep look at IBM’s new z13 mainframe. In August it announced LinuxONE – the most comprehensive effort yet to bring the value of mainframes to enterprises building Open Source solutions. In this bulletin we’ll look at what IBM has announced and how it will affect the Linux and open source world. Read more »

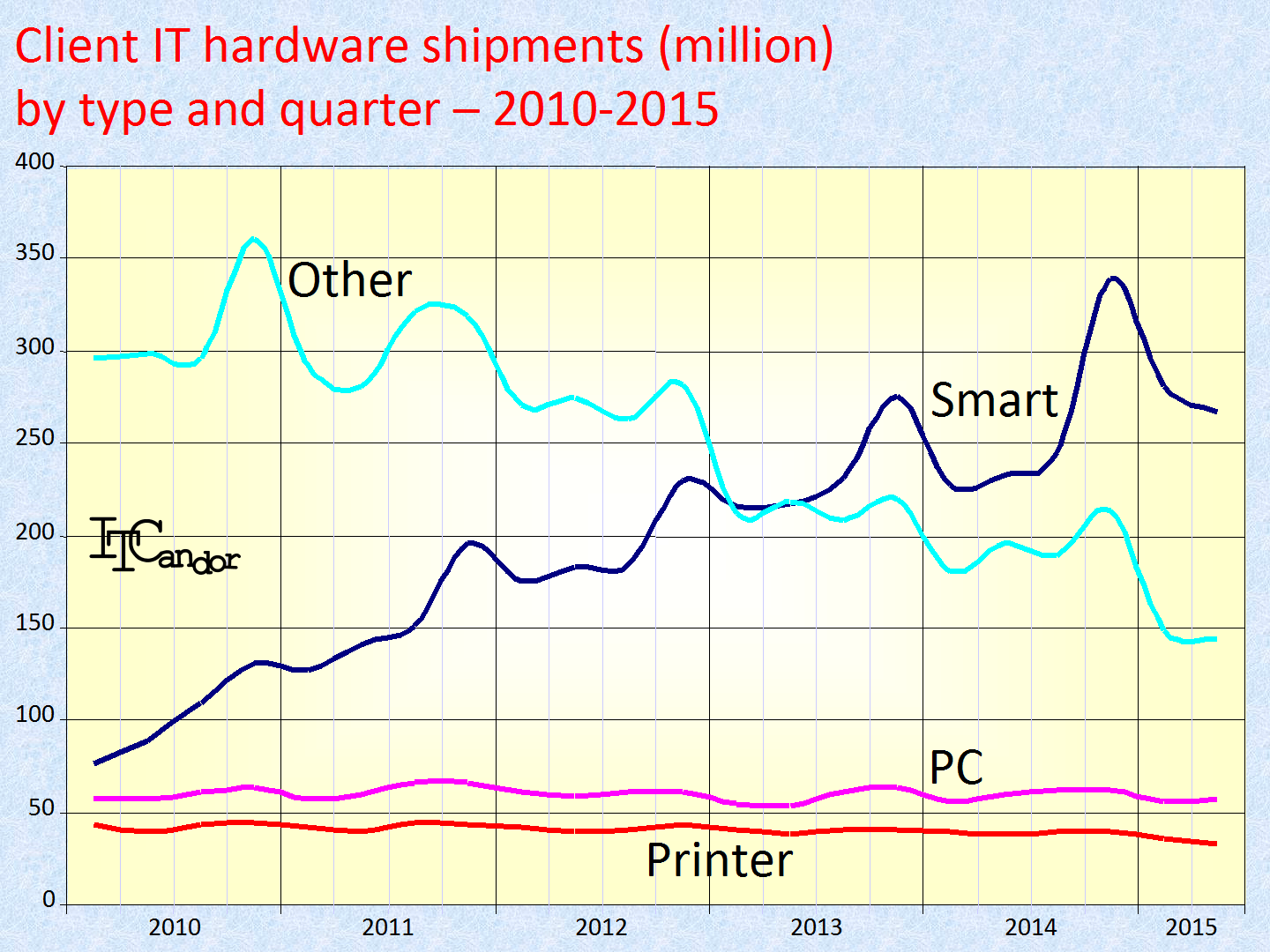

Client IT hardware devices – the shipment perspective

Following our analysis of market shares for client devices by type last week, I wanted to share the shipment perspectives with you. This bulletin is designed for those of you who these markets measure success and opportunities in unit terms. In total there were 2.2 billion shipments of client hard devices in the year to the end of June – up 2.1% on the previous year. Smart devices predominate (see the Figure), having overtaken ‘other’ devices in 2013. See my earlier article for definitions of what’s included there. Read more »

Client IT hardware devices up 4.6% in the year to June 2015

Last week we looked at enterprise hardware, so I thought it was time to look at client devices. This is a much larger market – worth $614b in the year to the end of June 2015. It grew by 4.6% in total. I’ve split the underlying categories into 4. Smart devices are smartphones, smart tablets, smart wearables (including anything running iOS or Android operating systems). PCs are desktop, laptop, PC tablets and workstations (including all machines running Windows on x86 chips). Printers are laser and inkjet (including Multi-Functional Printers, but excluding dedicated copiers). Others are digital cameras, basic mobile phones and audio and media devices. I’ve included all product sales, irrespective of the type or size of user. Needless to say we can split them out in greater detail. You’ll want to know more about how these markets are developing. Read more »

The enterprise hardware market falls 2.1% in Q2 2015 – is going server-centric

I’ve been looking at the enterprise IT market over the last couple of days, combining server, enterprise network and storage system numbers together mainly to assess market growth and vendor successes. With the server market growing, storage systems declining and networks somewhere in the middle it looks to me as there is good evidence that we’re moving to a server-centric world. Software running on servers is taking chunks of money out of the dedicated array market now… and will do the same to dedicated network hardware in the future. You’ll want toread more about the market movements and vendor shares. Read more »

ITC spending -5.5% in Q2 2015 – we’re in another downturn

I’ve just finished assessing the revenues of 150 separate IT and C vendors and am sorry to report that their results continued to worsen. In fact the total market declined by 5.5% to $1.5T in Q2. For the year to the end of June the market was down 2.8% to $6.1T. The Figure shows my forecast for each of the 4 contributing categories on a rolling 4 quarter basis to the end of 2016. In the year to the end of June hardware was up 0.4%, IT service down 1.5%, software up 0.2% and telecom service down 6.5%. For the quarter itself, everything was down – hardware by 0.1%, IT service by 3.7%, software by a staggering 6.5% and telecom service by 5.5%.

I know you’ll want to learn more, especially about the links with China’s economic troubles and the turbulent movements of currency I’ve been reporting for some time. Read more »

Toshiba’s woes and the Japanese triple whammy

Toshiba apologised yesterday for over-reporting its income statements from 2008 onwards, having delayed calculating its full-year financial results and setting up an independent investigation panel back in May. You’ll want to think more about its position as a Japanese vendor and global supplier. Read more »

BRUNS-PAK – a classical Data Center design consultancy

I had great fun talking to Mark Evanko – principal engineer of BRUNS-PAK – a short while ago. I’ve spent a lot of time in the last year evaluating the technical consulting activities of a number of larger vendors (see the Figure for some stats on the largest IT services companies) as well as writing a paper on migration/relocation, so it is very interesting to see what this specialist vendor is doing. Mark is amused about me being an Oxford Classicist – so let me rise to the challenge and give some appropriate analysis! Read more »

Mobile device revenues up 17% in Q1 2015 – Chinese suppliers surge

I’ve been busy adjusting my mobile device model to accommodate the growth of new form factors – ‘Smart Wearables’ and ‘IoT Devices’. although they’re not yet shipping in multi millions, I want to be prepared. In the process I’ve made a number of changes to my smart phone, smart tablet and basic phone research, which I publish here for the first time. You’ll want to think about the implications of these very large numbers. Read more »

Dell Strategy – get ready for the ‘digital economy’, the ‘API economy’

I had the excellent fortune to attend Dell’s 5th annual Dell Annual Analyst Conference (DAAC) forum last week to hear from Michael and his team about the company’s latest achievements. I’m following Dell more closely than ever now, reviewing its actions and strategy in a turbulent market. You’ll want to learn more about how it’s positioned to take advantage of future opportunities. Read more »

I had the excellent fortune to attend Dell’s 5th annual Dell Annual Analyst Conference (DAAC) forum last week to hear from Michael and his team about the company’s latest achievements. I’m following Dell more closely than ever now, reviewing its actions and strategy in a turbulent market. You’ll want to learn more about how it’s positioned to take advantage of future opportunities. Read more »

Amazon publishes AWS stats – a fat, growing, profitable business

Amazon has been quite secretive when it comes to breaking out its revenues – for instance it has never told anyone how many Kindles have been shipped. However in its Q1 results it decided to split out the revenues and operating income of AWS for the first time. I’ve estimated both by quarter, showing them in the Figure, using a rolling 4 quarter analysis. You’ll want to think about the consequences for the growth of cloud services in general and IaaS in particular. Read more »

Symantec’s simpler, more integrated, capacity-priced Backup Exec 15

Barnaby Wood, Senior Manager, Solutions Marketing joined Veritas 15 years ago – before Symantec acquired it. He thinks of the announced spin-off and recreation of the Veritas name as ‘coming home’. Backup Exec (BE) is a key software solution for backing up, archiving and restoring data. It has 2.2m (typically) SMB and mid-range customers, while Symantec’s Enterprise customers tend to use NetBackup. I thought you’d like an update from the discussion we had recently. Read more »

Barnaby Wood, Senior Manager, Solutions Marketing joined Veritas 15 years ago – before Symantec acquired it. He thinks of the announced spin-off and recreation of the Veritas name as ‘coming home’. Backup Exec (BE) is a key software solution for backing up, archiving and restoring data. It has 2.2m (typically) SMB and mid-range customers, while Symantec’s Enterprise customers tend to use NetBackup. I thought you’d like an update from the discussion we had recently. Read more »

Falconstor’s 15-year head start in SDS

FalconStor’s president and CEO Gary Quinn will ring the NASDAQ closing bell yesterday to celebrate the company’s 15-year anniversary. The company has simplified its market approach by launching Freestor – a product claimed as ‘the first truly horizontal, software-defined storage platform for unified data services’. You’ll want to learn more about this innovative company, which has always taken a ‘software-only’ approach to storage virtualisation and management. Read more »

FalconStor’s president and CEO Gary Quinn will ring the NASDAQ closing bell yesterday to celebrate the company’s 15-year anniversary. The company has simplified its market approach by launching Freestor – a product claimed as ‘the first truly horizontal, software-defined storage platform for unified data services’. You’ll want to learn more about this innovative company, which has always taken a ‘software-only’ approach to storage virtualisation and management. Read more »