Q1 2012 Server Update

- Q1 was surprisingly buoyant, although the worsening economy threatens a decline in coming quarters

- The market grew 1% to $15.3 Billion in the quarter

- $60 Billion in the year

- Unit shipments were 4 million in the quarter

- The installed base reached 44 million

- x86 servers 2% growth ($11.5 Billion) in the quarter

- 4% x86 growth to $44 Billion in the year

- Windows operating systems were 66% of revenues, Linux – 9%

- A drop in IBM System z revenues set back the rise in virtualised servers

- Virtualised server represented 37% of revenues: physical-only machines 63%

- Revenues declined 2% in the Americas

- Asia Pacific revenues grew by 2%

- EMEA grew by 1% in local currency

As it’s one of our most popular subjects, we thought you’d enjoy an update of our market sizing for servers. As with other statistical information on this site the data here is drawn form the ITCandor market model and is available in pivot table format if you want to investigate market share movements at a country level. We trust you’ll find this information useful for business planning and purchasing decisions.

The Total Market Dropped 1% For the Quarter And Year

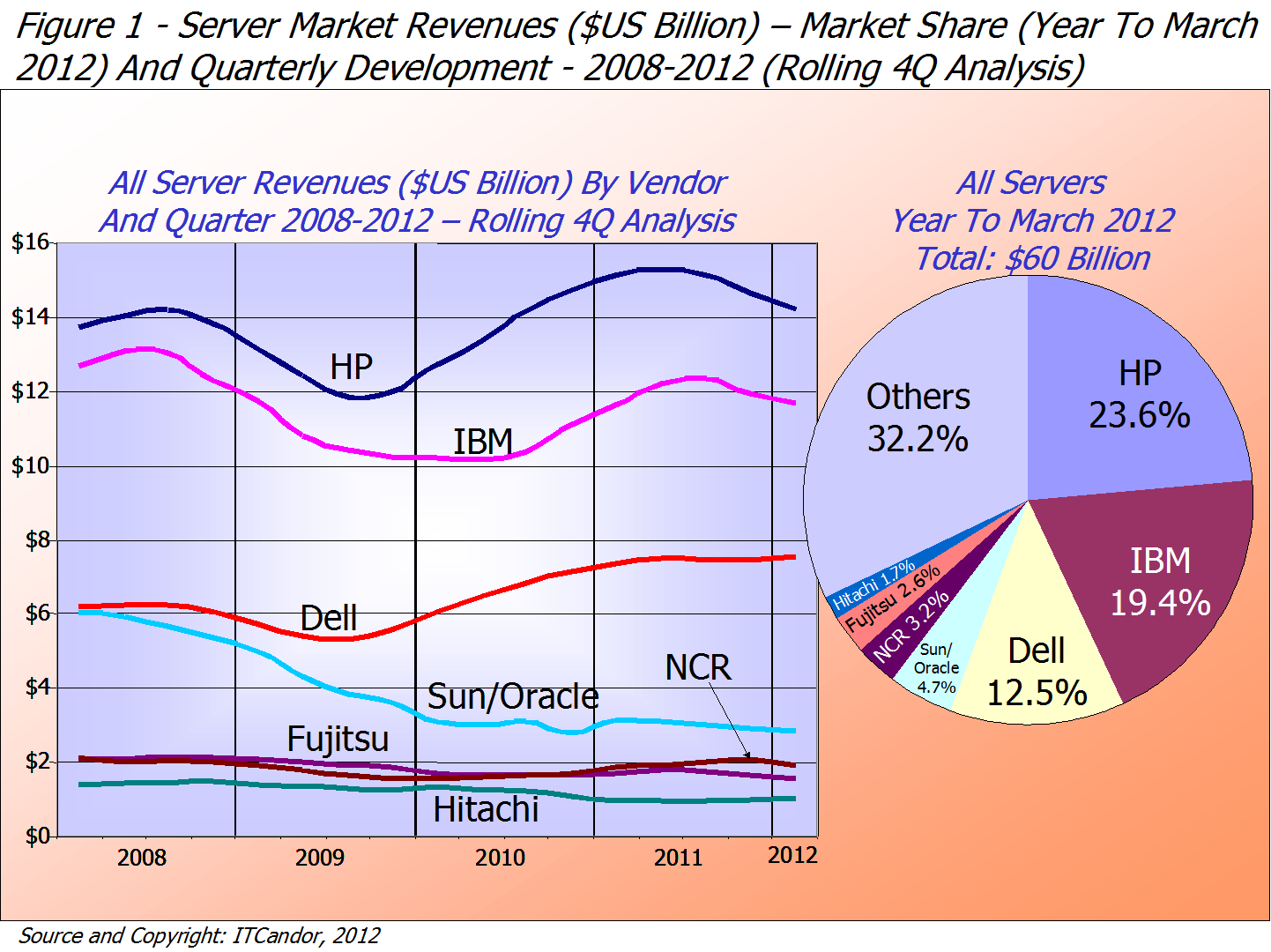

The server market was worth $15.3 Billion in Q1 2012 and $60 Billion for the year leading up to it (see Figure 1 for quarterly revenues by major vendor and market share). Unit shipments were 4 million, with the worldwide installed bases standing at 44 million by the end of the quarter. HP remained on top with a 23.6% share, compared to IBM in second position with 19.4%. Dell is in a clear third place – its 12.5% share is more than twice that of Oracle/Sun in fourth. HP (-11%), Oracle/Sun (-10%) and IBM (-8%) all experienced a decline in revenues, while Dell grew 4% in the quarter: Cisco, Hitachi and NEC also grew revenues. The market is poised between the strong recover of last year and the worsening economics of the coming Euro Crash.

{kind=link}

The x86 Server Market Grew 2% In the Quarter, 4% In The Year

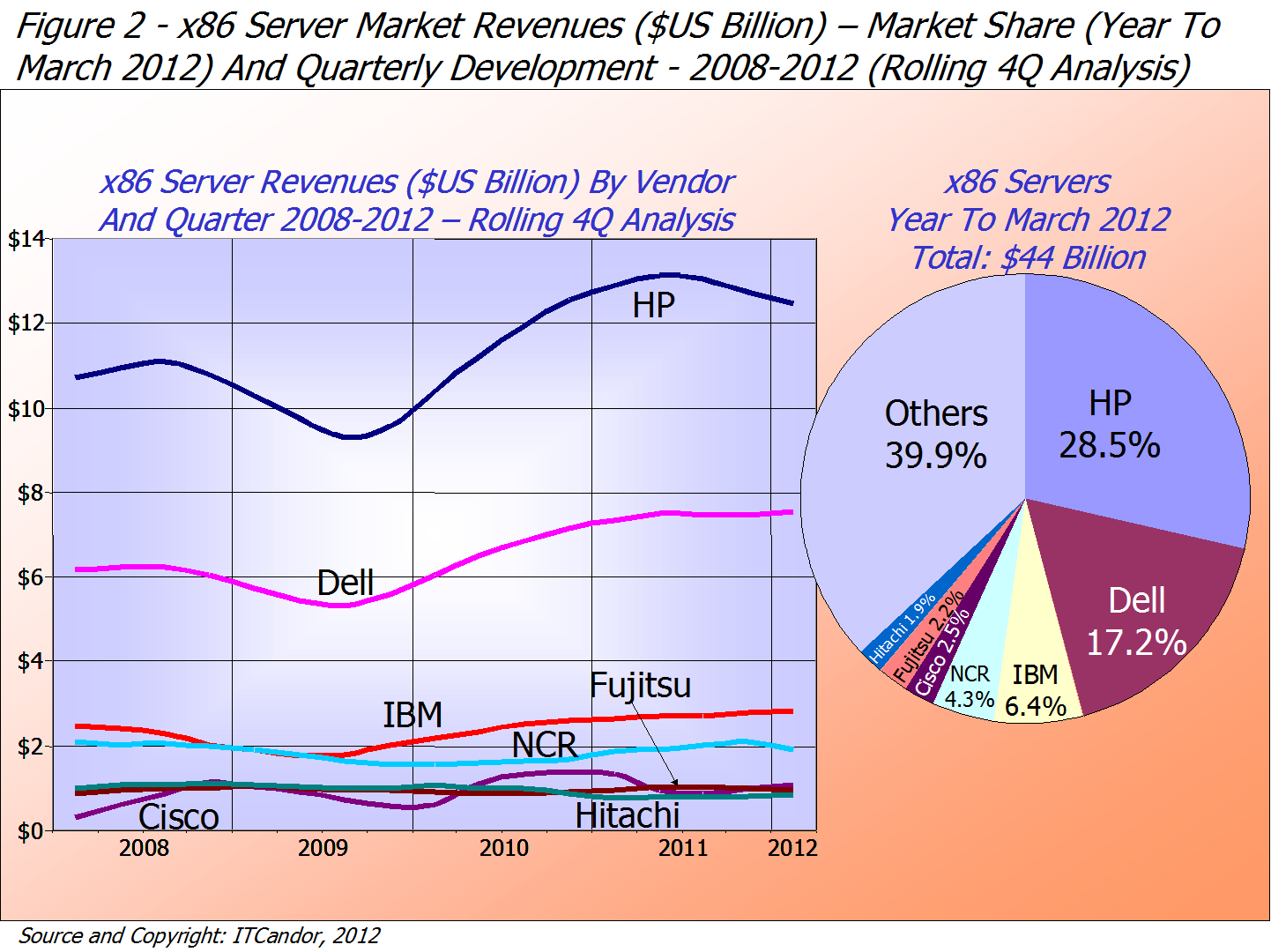

The x86 server market was worth $11.5 Billion in the quarter and $44 Billion for the year, growing at 2% and 4% respectively. While reviewing Intel’s new Xeon E5 processor, we noted that the market in Q4 had reached a hiatus as users waited for the new products. While the x86 market has returned to growth, it is a long way off the 22% in Q1 a year ago. Figure 2 shows market shares and the development of leading supplier x86 server business since 2008.

HP’s lead is stronger here (with a 28.5% share) than in the overall market, where IBM’s System z mainframes and AIX Power servers give it a much stronger position. Dell is in second place (17.2%), followed by IBM (6.4%) and NCR (4.3%). HP’s 8% decline in business may be related to its late announcement of Intel’s new chips and (even) the disruption of internal management changes. Cisco continues to show strong growth in ‘compute nodes’, although it remains a second-tier player.

{kind=link}

x86 Extends Its Lead Over Unix And Mainframe

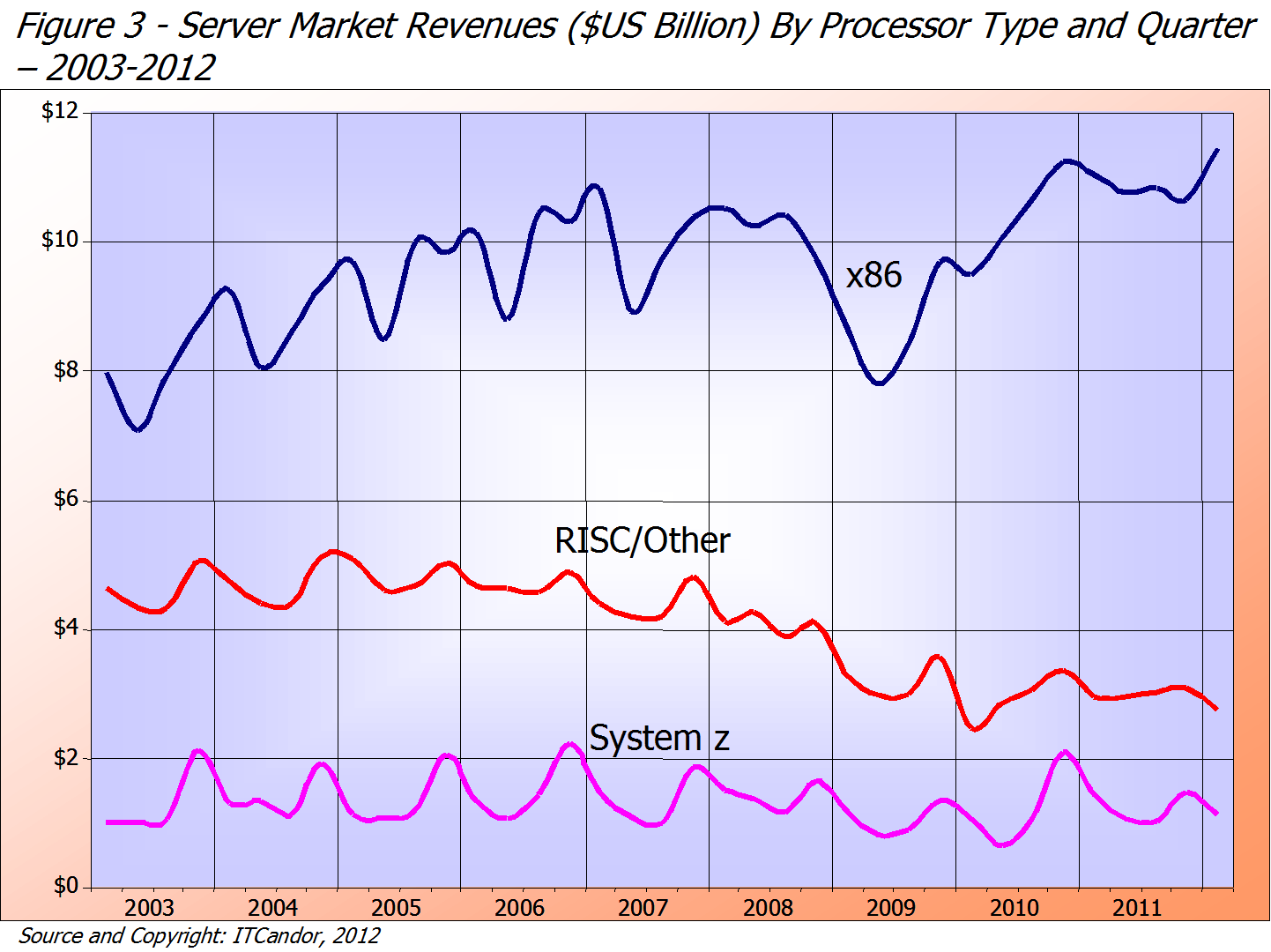

The Credit Crunch accelerated the movement away from Unix towards x86 servers, which has continued ever since (see Figure 3 for a view of quarterly revenues). x86 servers accounted for 75% of total revenues I the quarter, while RISC/Other dropped to just 18% of the market: it’s a shame that Oracle and HP aren’t doing as good a job as IBM at promoting the positive benefits of RISC processors. This sector will no doubt recover somewhat as ARM-based Micro Servers begin to ship. IBM’s System z revenues were down 21% in Q1 2012 to become 7% of the total server mix; this time seasonality and the significant growth of last year has affected the business.

{kind=link}

Windows And Linux The Clear Operating System Winners

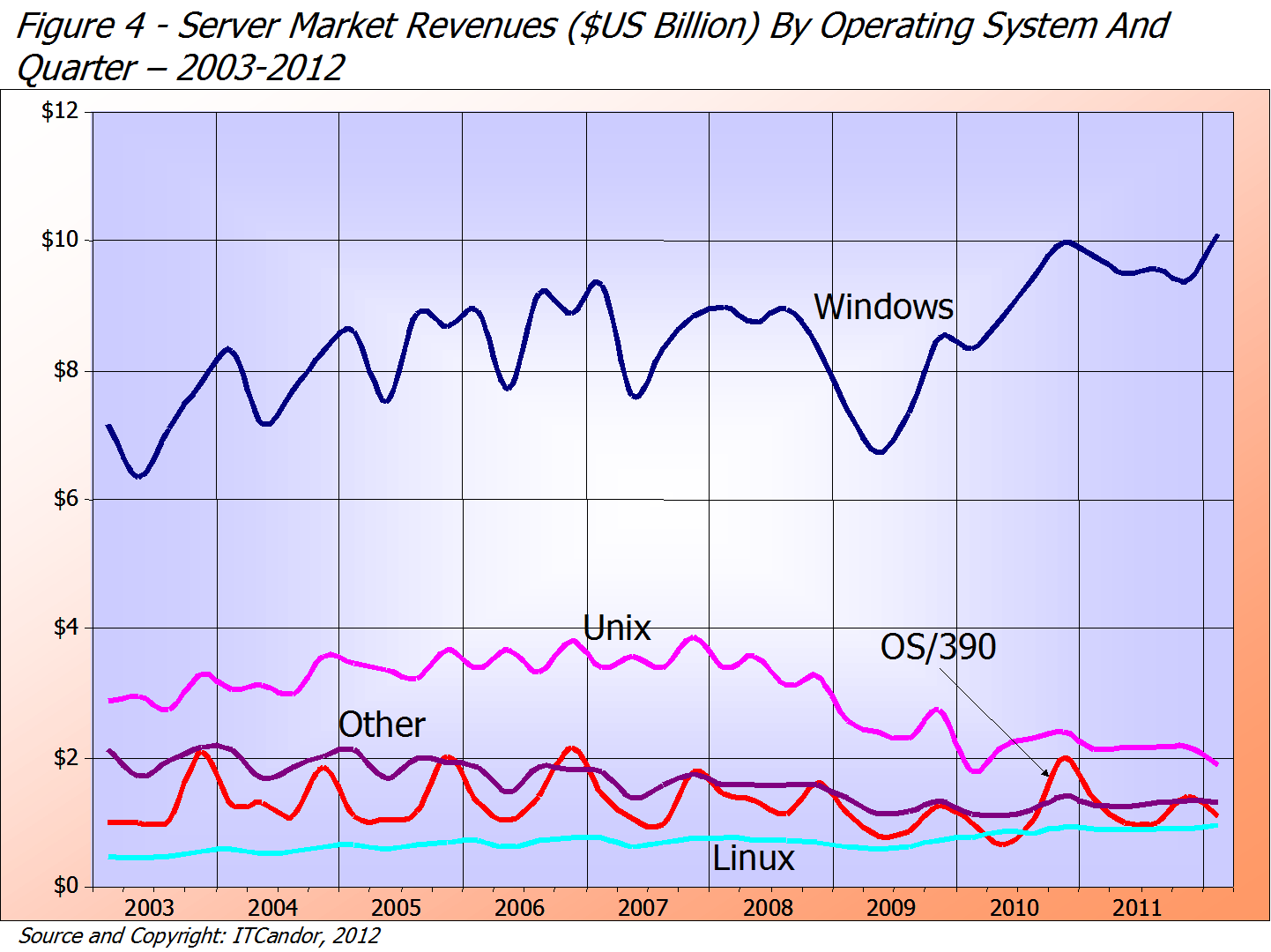

Operating systems are strongly tied to chip type, with Windows the clear winner in the server market following the downturn of the Credit Crunch in 2008 (see Figure 4). In Q1 2012 it accounted for 66% of server revenues, growing 4% to $10.1 billion. Linux also grew (6%), but represents only 9% of the market ($954 million): it is experiencing a slow continuous growth and is being used as the operating system of choice for large public Clouds. IBM’s OS/390 is exclusively tied to its System z systems and processor type. Unix shows a decline not only on RISC and Itanium chips, but also on x86, where Oracle/Sun’s Solaris operating system is no longer a choice for other vendors’ servers.

{kind=link}

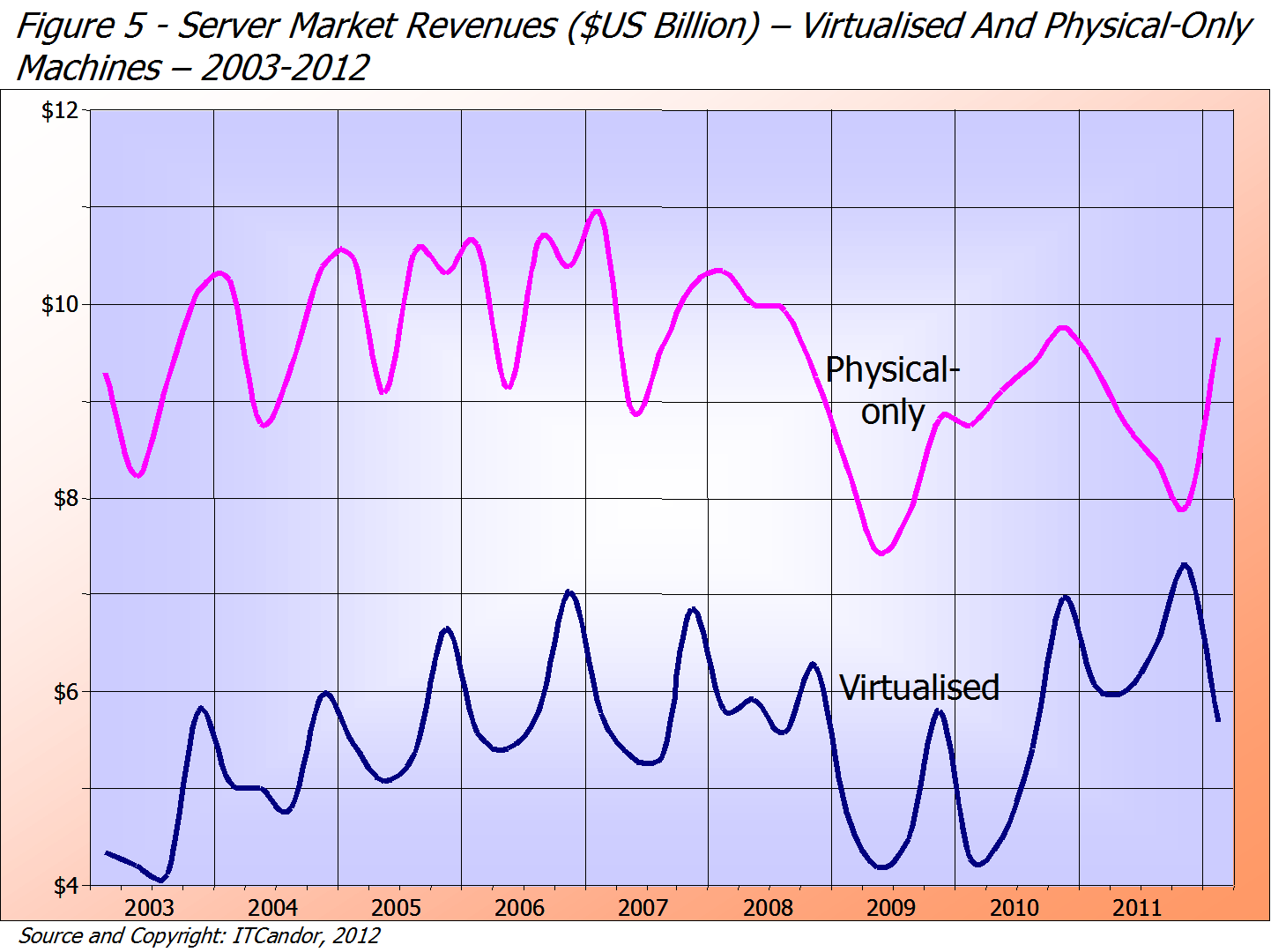

Declining IBM System z Revenues Set Back The Rise Of Virtualised Servers In Q1 2012

Virtualised servers represented 37% ($5.7 Billion) of server revenues in Q1 2012, which was a decline of 6% – due almost entirely to the fall of in System z (all virtualised of course) revenues – see Figure 5. The rise in x86 virtualisation has offset the fall off in Unix revenues over time, with proportions are now average in the 40%s as opposed to the 30%s back in 2003. You should not mistake the significant rise in x86 virtualisation driven by VMware’s ESX and Microsoft’s Hyper-V hypervisor usage as an indication that physical-only servers are being marginalized: it’s really just a movement in processor type from mainframe and RISC.

{kind=link}

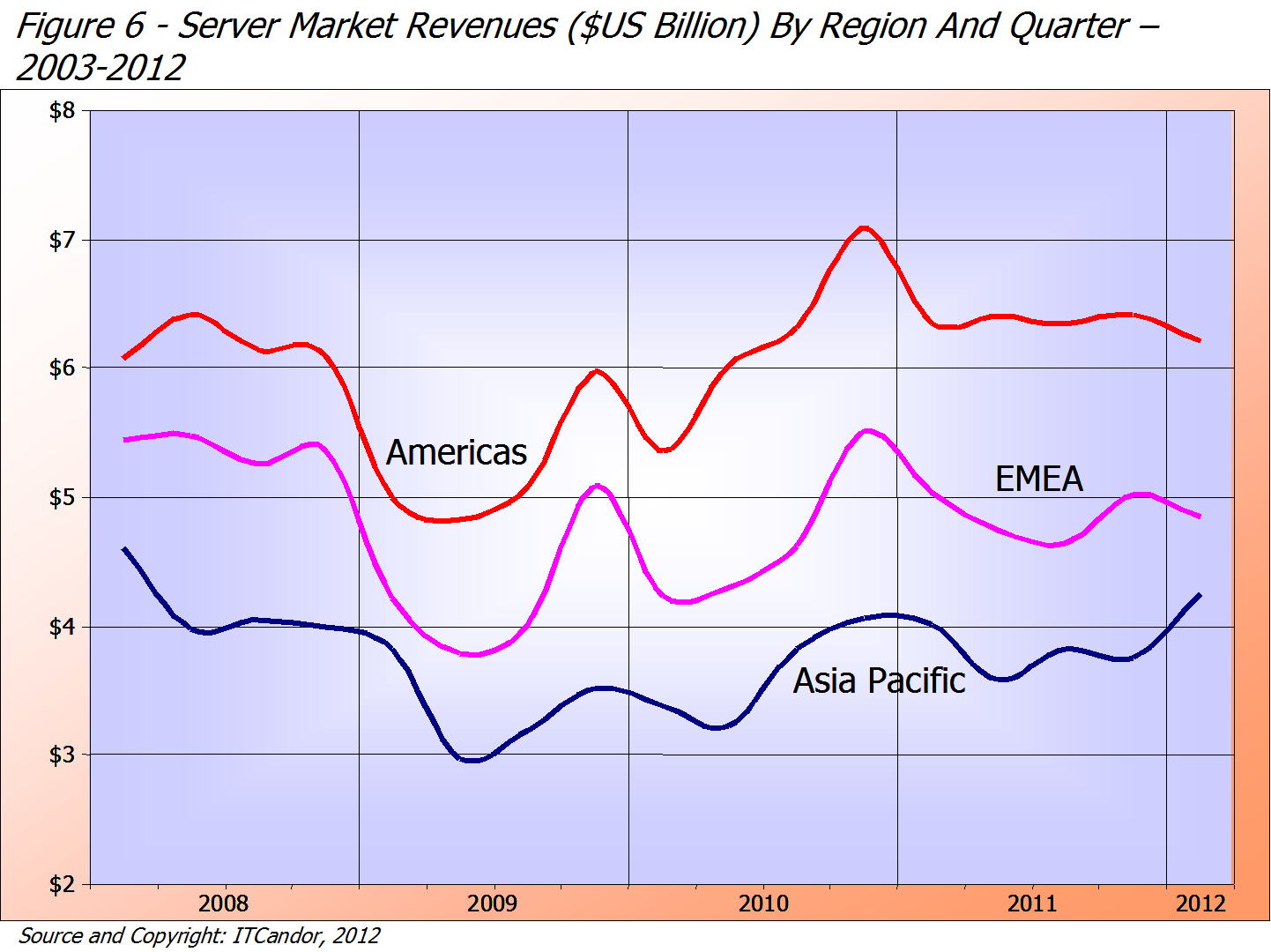

Server Business Is Strongest In The Americas, Although Asia Pacific Sees The Strongest Growth

The relative positions of regions in server spending have remained consistent over time, with the Americas accounting for 41% ($6.2 Billion) in Q1 2012 (see Figure 6): EMEA is the next strongest region, accounting for 32% ($4.9 Billion), with Asia Pacific third at 28% ($4.2 Billion). Growth in Q1 2012 varied significantly, with the Americas declining by 2%: Asia Pacific grew by 6% (2% in local currency): EMEA declined by 3%, although it grew by 1% in local currency. As in many other ITC markets Asia Pacific is catching up because it is less saturated. We expect to see declines in EMEA in the near future as a result of the Euro Crash (especially if Greece and/or other countries leave the Euro).

{kind=link}

Some Conclusions – A Surprisingly Buoyant Server Market – But Threatened

We certainly didn’t expect the first quarter results to be as strong as this, predicting that server spending would be badly affected by the worsening economy in most mature country markets: however, unlike in 2008, there has been no sudden loss in business confidence – no surprise at how badly GDP growth and government debt has become. Servers are also extremely relevant in a market becoming ever more centralised and turning to hosted applications, whether in the smart phone and tablet area or for corporate Cloud services. In addition the server market is not directly threatened by consumer spending, since the product type is currently exclusively used in businesses. Over coming quarters we expect to see a rise in Micro Server introductions (machines based on ARM and Atom chips) and an increase in spending on x86 machines as Intel and AMD’s new products come to market. While HP and IBM’s businesses are in decline, we don’t expect Dell to catch up in the near future.

We hope you enjoy this article. Please contact us if you need more at a country, regional, channel, vertical or customer size class level: similarly if you need unit shipments and installed base numbers – it’s all part of our model.

Lovely summary. Interesting to see those long term graphs in fig 6. AP does seem to have a much more “relaxed” trend – less pointy peaks.

Thanks Karl

To be honest I’ve smoothed them a bit – but you can still see the bigger Q1s in A/P, which is due to Japan.

Best – Martin

Hi!

!!Confused!! Could you help me here Martin? OpenSource Server O/Ss are free so their comparison to MS and other proprietal O/Ss by value should be 100% to nil.

(I understand “update” services and support services may confuse matters..)

I am very sensitive to MS being blown up as a business or as a Cloud success story when it is the current anti-thesis to public Cloud and Android OpenSource O/S.

I will continue to study your excellent MR article , now that I have spent my rage!

Rich K

My reasoning.

For example, annoyingly it still looks like “the world is MS” while the company continues to loose ground with many competitors and has lost real medium to long term strategy direction.

A very iffy prediction by “market watcher” company IDC (see P50 Information Age June 2012 issue or Google it) says MS will move from 1 or 2% of Smart device market (a fair number of MS employees there!!) to 19.2% in 2016, mainly at Androids’ cost in market share.

Found link :http://www.forbes.com/sites/ericsavitz/2012/06/06/windows-phone-to-top-ios-market-share-by-2016-idc-says/

This is very, very unlikely to be true!

(As the poorer world states pay a few dollars for their new/refurbished Smart devices and they are in the billions in number.)

My point is, it doesn’t really matter that in the short term today Apple and MS/Nokia are making $billions in profits, if in the medium to long term Android becomes the 90+ % market leader by unit and their very survival in this arena becomes bleak.

(As we foretell, depending on how many $billions in PR and marketing are spent by MS/Apple/Google.)

Rich K

Rich

I can’t comment much on the stats from my erstwhile employer: however the scenario for Microsoft OSes on smart phones is less positive than iOS or Android, but we expect growth – see http://martinhingley.files.wordpress.com/2012/06/phone-q112-fig3.png.

Best

Martin

Rich

You make ver valid points, especially as Red Hat is now a $1b company.

I assess the number value of server hardware running each OS – I should make that clear. It’s difficult, but I’ve been doing it for 3 decades. Microsoft’s operating systems are challenged everywhere – but much less so in servers.

best – Martin

Hi!

I am getting confused with the server vendor definition. We are major server critical component supplier, but it seems that we never put NCR as a major server vendor (we do POS business with NCR, but not in server products.) Could you help to clarify this?

Thanks!

Moulder

We consider NCR as a very important server vendor – see the market shares in the post. we’ll try to provide more coverage in future.

Best Wihes

Martin

Thank you for reply!

Does NCR participate in x86 server market? or they play in RISC server market? I am wondering which form factor they major in as well.

Moulder – they’ve been exclusively an x86 server vendor for many years.

Best – Martin

Does anyone know just how many organizations/businesses are purchasing x86 servers? That is, how broad is the market in terms of its customer base? Thanks! G

Greg

A very good question. x86 servers definitely have the widest spread in terms of business sizes buying them. 10 years ago they were spread more towards small and medium businesses, but their adoption by public Cloud and the advances of hypervisors make them much in demand by large organisations as well. IBM z and Power, HP Itanium and Oracle Sparc machines have always been – and still are – more popular in large and medium companies. The Credit crunch and on-going economic gloom has been accelerating the growth of x86 machines – and reduction in Unix – in larger companies from 2008. We’ve got some stats on this which we will share soon.

Best Wishes

Martin